Assessing the Economic Impact of India’s UPI

By Piyush Gupta & Chirag Chopra

India’s robust digital public infrastructure has played a pivotal role in enabling the country’s digital transformation, providing citizen-centric and transparent governance services, and facilitating breakthroughs in various fields, such as the DigiLocker, an online repository of citizens’ documents.

India has made significant progress in developing its digital public infrastructure (DPI). DPI refers to the digital systems and services that are available to the public, provided by government or public entities, and operated under a set of enabling rules, to enable the delivery of public services and facilitate economic activity. Some of the notable achievements of India’s DPI include the creation of Aadhaar, a unique biometric-based identification system, and the launch of the Unified Payment Interface (UPI), a real-time digital payment system that has revolutionised digital payments in India.

India’s robust digital public infrastructure has played a pivotal role in enabling the country’s digital transformation, providing citizen-centric and transparent governance services, and facilitating breakthroughs in various fields, such as the DigiLocker, an online repository of citizens’ documents. Furthermore, the digital infrastructure played a significant role in enabling the country’s response to the COVID-19 pandemic, with the Aarogya Setuand CoWin apps helping to track and contain the spread of the virus and facilitate the vaccination of a large number of people in a short period.

When we talk about digital public infrastructure, UPI is something which needs to be specially mentioned for the impact it has generated. The Unified Payment Interface (UPI), launched by the National Payments Corporation of India (NPCI) in 2016, enables citizens to transfer money from one bank account to another instantly. UPI has revolutionised digital payments in India, enabling individuals and businesses to make transactions seamlessly and securely.

Over the years, payment methods have evolved significantly as technology has advanced and societal preferences have changed. From bartering and using precious metals as currency to the introduction of digital payments, the way we pay for goods and services has undergone massive transformations.

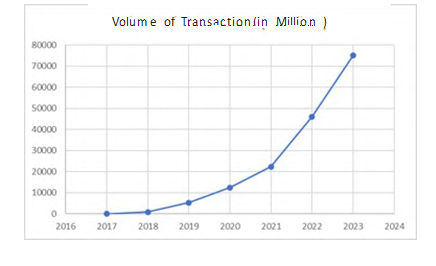

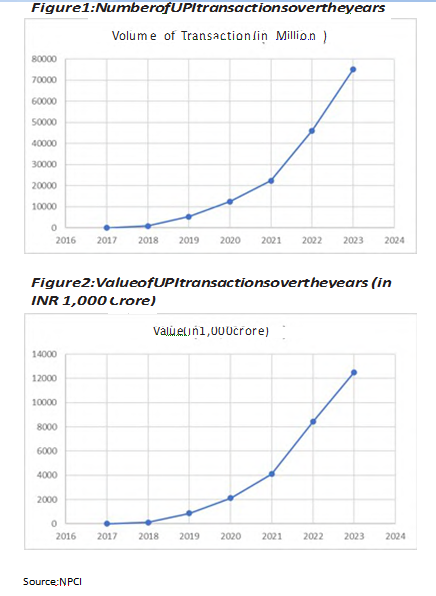

The UPI is a prime example of this as it has seen tremendous growth over the years, with over 8 billion transactions, worth INR 12.98 lakh crore, processed in January 2023 alone (approx. 3,100 transactions per second), this is a 75% Y-O-Y increase in terms of the number of transactions. In fact, as per there port published by ACI Worldwide in 2022, India leads globally in terms of real–time payment transactions with 48.6 billion transactions processed in 2021. It is interesting to note that China is in second position with only 38% of the real-time payment transactions processed in India in the same year.

UPI has initiated a significant behavioural change in the Indian populace as small and micro transactions, such as purchasing a cup of chai for INR 10 or buying a bag of fresh vegetables for INR 150, are increasingly being conducted through digital payments.

However, despite the significant in- vestments made in the development of digital public infrastructure in India, there is limited research on the impact of these initiatives.

Therefore, to understand the impact of UPI in India, we under took primary research using surveys of UPI users from all age groups across the country including Tier-1 and Tier-2 cities.

The study aimed to estimate the monetary savings by using UPI over other prominent methods and assumes that the money transacted through UPI would have been still transact-ed but by another method with a different cost to the economy. This economic cost is being measured in the study by taking into account the costs of transactions such as the Merchant Discount Rate (MDR) fees of credit and debit cards, costs of UPI transactions, and the cost of printing currency notes.

However, despite the significant investments made in the development of digital public infrastructure in India, there is limited research on the impact of these initiatives Therefore, to understand the impact of UPI in India, we under took primary research using surveys of UPI users from all age groups across the country including Tier-1 and Tier- 2 cities.

The study aimed to estimate the monetary savings by using UPI over other prominent methods and assumes that the money transacted through UPI would have been still transacted but by another method with a different cost to the economy. This economic cost is being measured in the study by taking into account the costs of transactions such as the Merchant Discount Rate (MDR) fees of credit and debit cards, costs of UPI transactions, and the cost of printing currency notes.

1,480 people responded to the survey from all age groups across the country. The survey assessed the preference of transaction medium of the people amongst cash, credit, and debit cards and we considered a range of first and third preferences for calculating a spread based on the total amount transacted through UPI till February 2023.

Till February 2023, approximately INR 300 lakh crore has been transacted through UPI methods. Based on our research and analysis, we estimate that this amount, if not transacted through UPI and transacted through cash, credit/debit cards, or other modes of payment, would have cost the economy approximately INR 5.5 lakh crore which can go to the extent of INR 7.2 lakh crore depending on the alternatives people have opted in the absence of UPI.

The cost of UPI transactions is taken into consideration and has been deducted to arrive at these savings. This implies that UPI has saved the economy approximately INR 5.5 lakh crore since its inception. This is a significant amount and highlights the impact of UPI on the Indian economy.

Moreover, the study also revealed that UPI has become the most preferred mode of payment in India, withover43%ofrespondentsstating that they prefer UPI over other modes of payment. The ease of use, speed, and security of UPI were cited as the primary reasons for its popularity.

In addition, it can be easily said that UPI has not only made digital payments accessible to all but has also enabled small and medium-sized enterprises(SMEs) to participate in the digital economy. By reducing the reliance on cash transactions, SMEs can now access formal credit and other financial services, thereby improving their competitiveness.

The effectiveness and large-scale impact of UPI can also be judged by the fact that it has become the most common medium of transactions in India as close to 300 million individuals and 50 million merchants are now using it and the system is also expanding its presence globally, with Singapore and the UAE being its latest adopters.

Author

Piyush Gupta is a Public Policy professional with a Master’s in Public Policy from the Lee Kuan Yew School of Public Policy, National University of Singapore and a Bachelor’s degree in Engineering from NSIT, Delhi. He has formerly worked with the Ministry of Electronics and IT (MeitY).

Chirag Chopra is an electronics and communication graduate from NSIT, Delhi and Delhi School of Economics (DSE) and has workedinmultipleBig4firmsinrisk advisory, government advisory and management consulting roles. He has also worked in a leading political consultancy firm.